Mortgage Professional America -- Clayton Jarvis

CBC Mortgage Agency announced it would be extending its Borrower Success Program free of charge to help borrowers impacted by COVID-19 ongoing disruption of the U.S. economy.

This topic consolidates the latest industry publications pertaining to natural disasters, including FEMA declarations, agency issuance's, and impact analyses from top industry providers.

Mortgage Professional America -- Clayton Jarvis

CBC Mortgage Agency announced it would be extending its Borrower Success Program free of charge to help borrowers impacted by COVID-19 ongoing disruption of the U.S. economy.

DSnews – Allen Price

Currently, there are multiple foreclosure moratoriums in place to avoid Americans from losing their homes during the COVID-19 crisis; many will likely continue to struggle financially when they end; however, servicers should be planning now for what happens when the smoke clears.

Search our Compliance Calendar for current regulatory changes & updates.

ABA Risk and Compliance

American Bankers Association President and CEO Rob Nichols urged banks to adopt a policy requiring anyone entering a bank branch to wear a mask or face covering to protect employees’ and customers’ health and reduce transmission of the COVID-19 virus.

Mortgage Professional America – Clayton Jarvis

SmartSearch, a U.K.based anti-money laundering firm, announced its arrival in the U.S. marketplace.

HousingWire – Alex Roha

In a virtual webcast hearing, the Financial Services Committee examine how services provided clarity and information on the CARES Act and forbearance options for borrowers.

FDIC is providing regulatory relief to financial institutions and facilitate recovery in areas of Michigan affected by severe storms and flooding from May 16, 2020 through May 22, 2020..

ACES ENGAGE 2025 registration now open!

Join us at the Broadmoor in Colorado Springs on May 18-20, 2025.

MReport -- Mike Albanese

Danielle McCoy is Fannie Mae VP, and Fair Lending Officer spoke on what the GSE is doing to help homeowners understand their options and recognize fraud during the COVID-19 crisis.

MReport -- Brian Kucab

Underwriting has seen an impact from COVID-19 that makes the day-to-day a bit more challenging and uncertain.

Mortgage Professional America – Ryan Smith

According to a new report from CoreLogic, early-stage delinquencies boosted the national mortgage delinquency rate to its highest level in more than four years.

Freddie Mac is introducing the Disaster Payment Deferral option, as well as expanding the definition of an “eligible disaster”, updating credit reporting for borrowers, and proving updates and reminders on servicer incentives, disbursement of loss proceeds to borrowers, EDR reporting, and escrow shortage repayment.

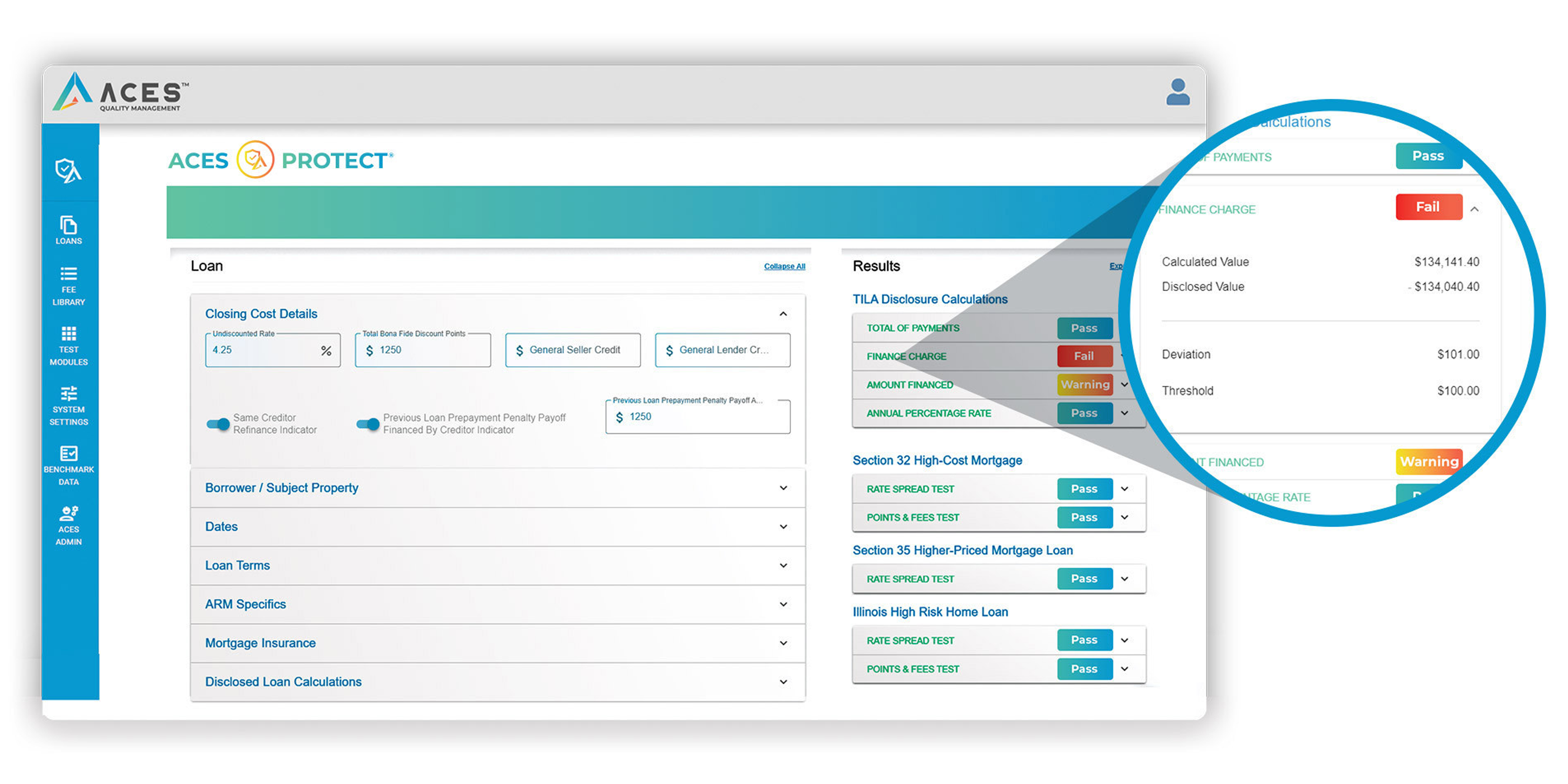

Automated compliance tests to ensure compliance on more loans in less time

Fannie Mae has updated LL-2020-08 to provide additional procedural instruction to servicers, including expectations pertaining to the July 2020 loan activity reporting period, the location of reports where pertinent information related to this process may be found in the month of August 2020, and the location of reports where pertinent information related to this process may be found beginning in the month of September 2020.

Fannie Mae has updated LL-2020-02 to clarify reporting requirements when a borrower impacted by a COVID-19-related hardship experiences another, concurrent hardship, and to address these new topics: disbursing hazard loss draft proceeds and impact of COVID-19 on Fannie Mae Home Affordable Modification Program “Pay for Performance” incentives.

Fannie Mae has updated LL-2020-09 to revise the retention workout option incentive fee table to incorporate the incentive fee for a disaster payment deferral.

Fannie Mae has updated LL-2020-07 to update the requirements for repayment of any escrow shortage amount identified in connection with a COVID-19 payment deferral or as part of the next annual analysis, clarify how servicing fees, guaranty fees, and excess servicing fees (if applicable) will be reimbursed for mortgage loans that receive a disaster payment deferral, and clarify that the servicer must evaluate the borrower for a Flex Modification in accordance with the reduced eligibility criteria when the borrower becomes 60 days delinquent within six months of the COVID-19 related payment deferral’s effective date and the servicer is unable to achieve QRPC.